As we enter one of the biggest tech IPO seasons in recent history — LinkedIn, with Groupon, Pandora, Zillow, Dropbox, Zynga, and CafePress all lining up behind it — it’s hard to know what will fly and what will flounder.

One indicator of a company’s potential is how well it can scale its business independent of human intervention. This isn’t simply the ability to automate tasks or replace workers with machines; rather, it’s the ability to augment people with data and processes.

Call it the Meat to Math ratio.

First, a comparison

To explain what I mean, I’ve done some back-of-the-napkin math on six companies. Four are public, and two have impending IPOs. Of the four public ones, two are disruptors and two are the established incumbents they’re beating to a fiscal pulp.

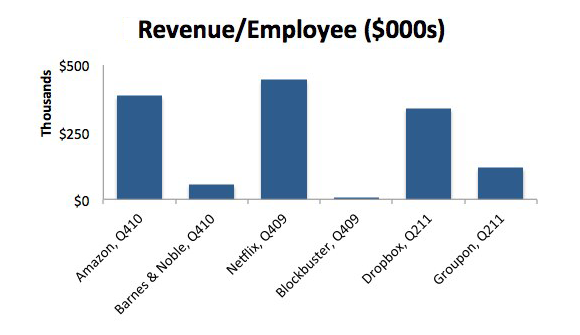

One common way to measure a company’s productivity is the revenue per employee.

It’s not just about revenue per employee, though. As Paul Strassman said before the first dot-com bubble in 1998, we shouldn’t give industrial-age answers to information-age questions. Rather, it’s about how well a company can leverage its employees over the long term. Companies with a good meat-to-math ratio should be able to do things like:

- Automating processes at scale.

- Maintaining genuine interactions with their customers despite a high number of customers per employee.

- Finding new businesses from their own data exhaust through introspection and experimentation.

I want to look at each of these three in more detail.

Turking, then automating

I’ve spent the last year looking at a lot of new ventures, partly because of my involvement in a startup accelerator. Our accelerator uses lean startup methodologies. These are techniques for pushing the uncertainty to the front of the company’s lifespan. Rather than getting your investment and business in place before launching, a lean model is all about doing the least amount of work to accurately predict whether a particular business will succeed. Then it’s about iterating quickly to a fit between a set of product features and a target market. It’s not a perfect science, but it’s a good way to avoid losing a lot of money on a bad idea.

One lean startup trick is doing things by hand rather than wasting time programming. Consider, for example, that you’re thinking of launching a search-by-email company. Rather than coding everything, you’d read users’ emails, search for them, and respond in an email. You’d soon find out whether people wanted to search by email, without investing time in natural language parsing, email handling, and so on. You’d be “turking,” a term that refers to the Turk (from which Amazon’s people-as-a-function-call service gets its name.)

Turking takes many forms. It might mean drawing rudimentary user interfaces, then watching someone “use” them with their finger (a process called paper prototyping). Or it might mean replacing some complex function with a human (what we jokingly refer to as a Flesh-Based API). Or maybe it’s creating landing pages for applications that don’t exist, to see who signs up. One of our incubated companies didn’t code for a month. Instead, they ran surveys and did customer development until they found something people cared about.

Early on, meat is cheaper than math.

Strata Conference New York 2011, being held Sept. 22-23, covers the latest and best tools and technologies for data science — from gathering, cleaning, analyzing, and storing data to communicating data intelligence effectively.

Strata Conference New York 2011, being held Sept. 22-23, covers the latest and best tools and technologies for data science — from gathering, cleaning, analyzing, and storing data to communicating data intelligence effectively.

But if a company can’t make a transition to math, it will have to turk at scale. Turking at scale is another way of describing the dirty business of managing people, with all of the chaos, uncertainty, and HR headaches it entails.

There’s an old adage among investors that a change in order of magnitude means a change in leadership. If a company goes from $10M a year to $100M a year in revenue, it’s time for a new leader. Similarly, if it goes from 100 to 1,000 customers, or from 10 to 100 employees, something has to change. Those customers and employees are meat, and meat is hard to scale.

Cloud computing and virtualization are a move from atoms to bits, replacing rack-and-stack with click-and-drag, and the resulting increases in IT productivity and server-to-administrator ratios are impressive. If you move to a virtualized, properly orchestrated IT architecture, you can survive an order-of-magnitude increase without throwing meat at the problem.

Put another way, meat is how you scale atoms — the kind that make up brick and mortar. Math is how you scale bits — the kind that make up big data businesses. Businesses that can scale bits are interesting, because bits don’t have the coefficient of friction that atoms do.

Being genuine to the masses

There’s a book called “The Clustering Of America.” At one time, it was the Bible of marketing. It broke down, zip-code by zip-code, the population of the United States. It clustered people into simple and almost laughably stereotypical groups like “Blue-blood Estates,” “Dodge Diplomats,” and “Towns & Gowns.”

It was the perfect book for a “Mad Men” era, where a pithy slogan and the right timeslot could open a million wallets. In the golden age of broadcasting, obedient audiences sat down as one around the family TV to watch a show at a time of the network’s choosing.

Today, that world is a fading memory. DVRs, iTunes, and streaming have freed us from the tyranny of the o’clock. They’ve also made it easy for us to find our niche programming. Bruce Springsteen didn’t think big enough: We have 57 million channels, and everything’s on.

Traditional marketers hate this. They’re hung over, recovering from a cheap cocktail of one-to-many, broadcast media purchases. They like buying things in big chunks, aimed at homogeneous clusters.

By contrast, modern marketing is about attention and engagement. It’s about doing something interesting, and getting tailored messages to micro-markets that expect personal attention and engagement with the companies they love. Every brand has its Little Monsters, but unlike Lady Gaga, legacy businesses don’t know how to interact with them.

Former Coca-Cola CMO Sergio Zyman describes marketing as “selling more stuff to more people more often for more money more efficiently.” In other words, selling at scale. If modern, post-broadcast marketing is about being genuine, then marketers face the challenge of being genuine (meat) at scale (math).

Companies that can work this out will win. But it will take big data systems, next-generation customer relationship management, and machine learning to help augment front-line employees.

Mining your own exhaust

Netflix and Amazon have something in common beyond their destruction of incumbents: the ability to create new businesses from whole cloth while still generating revenue. Netflix managed to become the dominant paid streaming platform, using mail-based distribution to bootstrap itself. Amazon created a cloud service from what it learned about running large-scale IT infrastructure; introduced a digital reader that now outstrips book sales; and expanded from books into many other retail markets.

Blockbuster and Barnes & Noble could have done these things, but they didn’t. Netflix and Amazon used their own data exhaust to innovate. They started new races in the middle of an existing one. As data-driven companies, they create volumes of data about their own operations, then recycle this into new insights and new businesses. Another reason for their agility is that meat has inertia: it’s hard and time-consuming to hire, fire, and retrain people; it’s easy to change an algorithm.

Back to those companies

So the meat-to-math ratio is vital for several things:

- Scaling the company without adding messy atoms and the related overhead.

- Scaling marketing without becoming disconnected from markets or customers.

- Iterating into new markets and new services adjacent to a core business.

Comparing our six firms — four public, two soon to be — in this light, what does a good meat-to-math ratio mean for your business? Let’s look closely at the two impending IPOs: Groupon and Dropbox.

Groupon’s offering, initially valued at $30B, is taking a beating. It has 7,500 employees, and it’s adding them fast. Despite the hiring binge, Groupon is seeing a promising increase in word-of-mouth sales, which is a sustainable model for scaling the business, and cost of customer acquisition is a key measure of whether a company can survive.

But Groupon has to sell to two groups: consumers looking for deals, and merchants willing to offer them. Humans have to call on small businesses directly. There are other reasons for Groupon’s troubles — the company lacks sustainable barriers to entry, as shown by competitors like Google and LivingSocial — but the root of the issue is this: Groupon is throwing meat at the growth problem, when it should be throwing math at it.

Dropbox, on the other hand, has 74 employees (a number that’s also growing fast, but is a hundred times smaller than Groupon.) Its IPO is valued at $5B, and it reportedly accepted a lower valuation in order to go with the banker it wanted. Dropbox has customer acquisition built into its model, a viral-marketing scheme where users invite their friends in return for extra free storage.

Assuming that the market values math over meat, how would you expect these two companies to compare on valuation per capita?

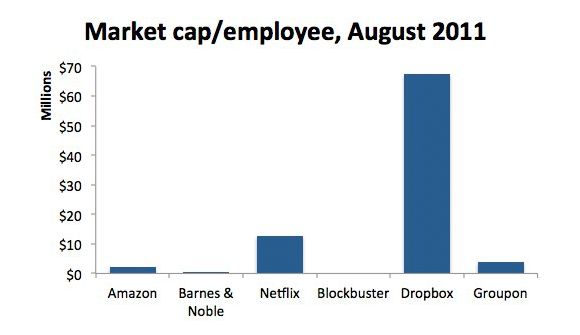

The way we keep score, like it or not, is market capitalization or IPO valuation. Let’s compare these six companies’ IPO values by company.

Clearly, if you’re proving you can scale with math instead of meat, the market rewards you handsomely.

In a data-driven world, the true measure of any organization, from a regional government to a global conglomerate, is its meat-to-math ratio. This sounds like a cold statement, saying machines are better than people. That’s not the point here: machines are better with people, and companies that can’t augment their employees with data and tools, that cling to antiquated ideas like broadcast, and that can’t turn their data exhaust into insight and innovation, are doomed.

Showing my math

The numbers I’ve used come from a variety of sources and time periods; they should be treated as illustrative, rather than hard data. In the interest of transparency, here’s how I got the data. If you have better numbers, I’d love to hear them.

For Amazon: Amazon had $12.95B in Q410 revenues (This includes a variety of other revenues, most significantly non-media sales and computing services), and 33,700 employees, meaning a revenue per employee of $384,273. The company had a market cap of $91.8B in early August, 2011, and roughly 43,200 employees, for a value-per-employee of $2,125,694. Sources: Google Finance; Techflash, Blorge.

For Barnes & Noble: $1.91B in Q410 revenues, and 35,000 employees, meaning a revenue per employee of $54,571. The company had a market cap of $947M in early August, 2011, and roughly 30,000 employees, for a value-per-employee of $31,567. Sources: Hoovers says 30,000 in 2011, Wikipedia says there were 40,000 employees in 2008, and Zenobank says 35,000 today.

For Netflix: $444M in Q409 revenues, and 1,000 employees, meaning a revenue-per-employee of $444,000. The company had a market cap of $12.8B in early August, 2011, and 1,000 employees, for a value-per-employee of $595.92M . Sources: Home Media Magazine; Netflix’s Adrian Cockroft tells me there are roughly 1,000 salaried contractors, plus hourly workers at distribution centres. I’m being conservative and using that same number for 2009, when it was certainly smaller.

For Blockbuster: $400M in Q409 revenues. The company peaked at 60,000 employees in 2009; I’ve assumed 55,000 by Q4, meaning a revenue-per-employee of $7,273. The company is not currently trading. Sources: Home Media Magazine, USNews.

For Groupon: Q211 revenues were $878M, with roughly 7,500 employees, for a revenue-per-employee of $117,067. The company’s IPO filing was initially valued at $30B, but will likely be significantly lower; nevertheless, I’m using the original valuation. That means a value-per-employee of $4M. Sources: Groupon S-1 filing; Business Insider says Groupon had 3,000 employees in Q4 2010, and is adding headcount aggressively. SB Online says hiring costs have jumped. And the best guess on Quora puts the count at 7,500 employees.

For Dropbox: In Q211 Dropbox had $25M in revenues, and 74 employees, for a revenue per employee of $338K. The company is planning a $5B IPO, which means a value-per-employee ratio of $67.6M. Sources: There are 74 employees on Dropbox’s website (they list them all.), TechCrunch suggests that the company chose a lower valuation than they could have in order to get the right investment bank. Business Insider estimates 2011 revenues at $100M total; I used 25 percent of these.

Related: